Liquity v2: BOLD Stability Pool opportunities

Robert Lauko

April 29, 2024

Liquity v2 is built to not only provide a unique borrowing experience, but to also offer a dynamic marketplace between borrowers and stablecoin holders looking to earn attractive yields.

The protocol will direct the lion’s share of its interest revenue to incentivize Stability Pool depositors (aka “Earners”), creating attractive and sustainable earning opportunities for BOLD holders. Funneling yield to single-sided depositors is a more capital efficient way of driving demand for BOLD than paying out LP incentives to token pairs on external AMMs.

Liquity v2 will behave similarly to money markets but with opposite spreads: depending on the utilization and integration of BOLD in the broader DeFi ecosystem, the Stability Pool will generally exceed the average borrow rates, something that isn’t possible on traditional lending markets where borrowers always pay higher rates than what the lenders receive.

This is because lending pools are unlikely to be 100% utilized, implying an unused portion of the funds which doesn’t earn any yield. A Stability Pool on the other hand only contains a portion of the entire stablecoin supply and is thus always smaller than the debt for which interest is paid. The more BOLD is circulating outside the pool, the higher the yield for depositors. With a growing number of external use cases, BOLD’s monetary premium will thus increase, benefitting its holders through higher effective interest rates.

Stability Pool and liquidations

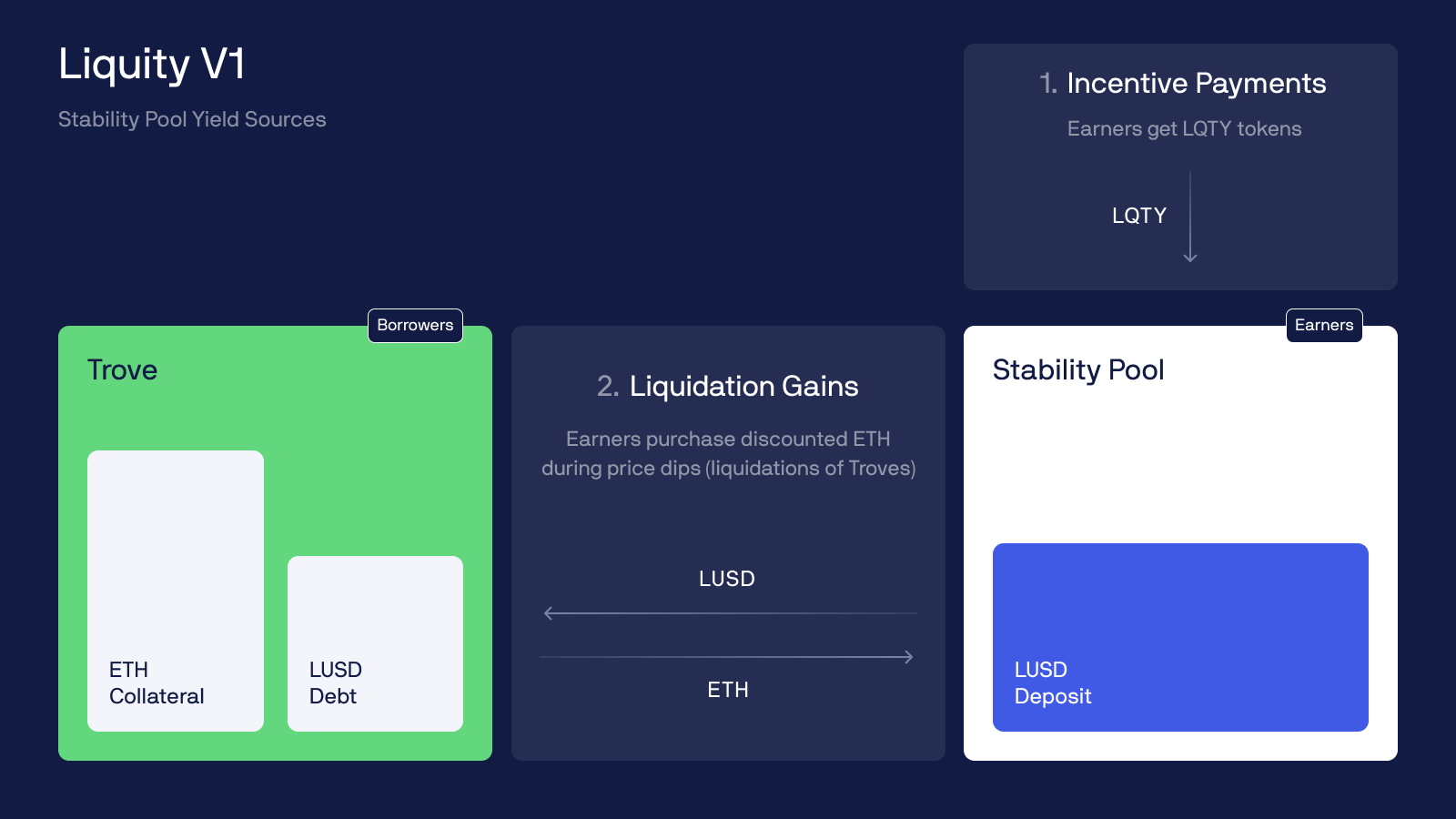

Building on Liquity v1’s achievements, the protocol harnesses Stability Pools for efficient liquidations of bad debt and to ensure overcollateralization. To recap, a Stability Pool (SP) is a smart contract that takes stablecoin deposits from holders, then uses the funds to repay the debt of “underwater” borrowers who exceed the liquidation threshold (maximum LTV).

In v2, depositors will receive a pro rata share of the liquidated collateral (at a discount) in exchange for the BOLD which gets burned in proportion to the size of their deposits. BOLD deposits will thus be partially converted into ETH or LSTs as liquidations take place. Given that liquidations are triggered at an LTV below 100% (e.g. 91% for wETH), BOLD depositors are set to make liquidation gains as the value of the received collateral will regularly exceed the lost BOLD by the 5% liquidation penalty which is stomached by the liquidated borrower.

In addition to liquidation gains, Stability Pool depositors in Liquity v2 (aka 'Earners') will receive around 70% of the interest paid by the borrowers (in BOLD) of the respective borrow market, making it the primary source of yield.

Multiple Stability Pools to manage risk across collateral types

Unlike Liquity v1 with ETH as its sole collateral asset, Liquity v2 incorporates multiple Stability Pools, one for each collateral type (LSTs / ETH). Every collateral thus forms a separate borrow market with its own set of borrowers and a corresponding Stability Pool.

Collateral risk is contained inside each group of borrowers (no mixing of collateral across borrow markets), while the exposure of depositors is primarily defined by the collateral asset they have opted for: by depositing BOLD e.g. to the wstETH (Lido) Stability Pool, you will obtain an exclusive interest share of wstETH-backed loans and liquidation gains in wstETH only, and no other collateral types.

However, as an overcollateralized stablecoin, BOLD ultimately remains dependent on all collateral assets, making collateral risk management particularly important.

Liquity v2 introduces several new mechanisms to contain and reduce risk from each collateral:

Separate Stability Pools: the separation into multiple borrow markets and Stability Pools allows the markets to establish their own range of individual interest rates and risk parameters.

An adaptive redemption mechanism: collateral perceived by the market as risky will be preferentially redeemed to ensure the exposure of the system to this collateral type can be reduced. This mechanism will be covered in a separate post.

These risk measures will be solely driven by market forces - there will be no need for external governance oversight.

Adaptive redemptions

The protocol’s exposure to each LST will be reflected individually through the ratio between the debt collateralized by the LST and the size of the respective SP backing it. For example, the SP for pure ETH may cover 60% of the ETH-backed loans, while the SP for wstETH may only account for 40% of the wstETH-backed debt. This metric enables the protocol to manage collateral risks in an autonomous way by directing BOLD redemptions towards LSTs with lower SP backing.

This mechanism is complemented by the fact that each borrow market will have its own redemption ordering based on the interest rates paid by its borrowers. In other words, your redemption risk as a wstETH-borrower would depend on the interest rates paid by fellow wstETH-borrowers, but not on the interest rates set by ETH borrowers for example (an article on this will be released at a later date).

Economic benefits of LST market segmentation

Due to this economic segregation, each market will establish its own range of interest rates reflecting collateral risk, opportunity costs and competition. For example, borrowers are likely to pay higher average interest rates for LST-backed loans than for loans backed by pure ETH.

Aside from just being a single stability pool depositor, users could also do more sophisticated strategies like the ones below.

The interest rate difference will impact the amount of funds deposited into each Stability Pool, allowing the protocol to converge towards APRs reflecting the exposure to LSTs with different risk characteristics.

Note that a smaller SP relative to its secured debt can achieve a similar or higher yield than a larger SP even if the average interest rate received from its borrowers is lower than the rates paid to the other SP. It all boils down to how big the cake is and how many pieces it is cut into.

To sum it up, depositors will have the choice to deposit their BOLD to several Stability Pools depending on the expected yield and their desired exposure to collateral assets. While some depositors may be chasing the highest yield, others may, for instance, prefer more established LSTs over smaller cap LSTs.

Creating sustainable yield generating opportunities is at the core of Liquity v2. As hinted upon earlier in this article, a portion of the fees that the protocol generates (~20%) is diverted towards incentivizing various LP pools with BOLD.

By enshrining protocol incentivized liquidity within the protocol, Liquity v2 aims to deliver predictable and sustainable yield opportunities with BOLD.

Questions?

Head over to our Discord.